In an increasingly digital economy, transparency and automation in taxation are no longer optional — they are essential. Among all the reforms implemented under the Goods and Services Tax (GST) regime in India, E-Invoicing has emerged as one of the most impactful.

This article explains who needs it, how it works, latest turnover thresholds, technical requirements, benefits, challenges, integration tips, penalties, and best practices to ensure seamless compliance — all backed by real-world context and actionable guidance.

Introduction: What is E-Invoicing Under GST?

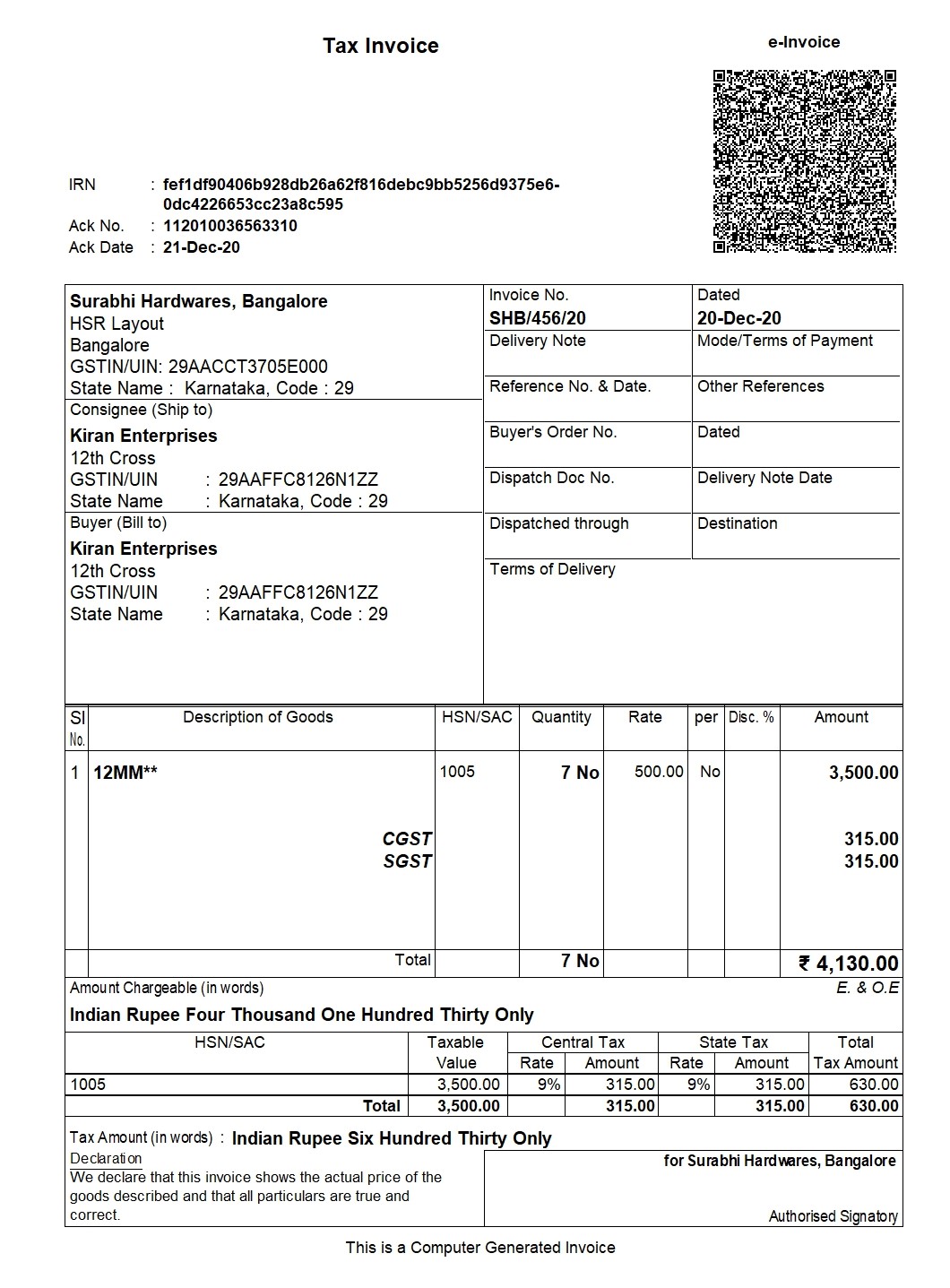

E-Invoicing (Electronic Invoicing) is the process of electronically reporting your business invoices to the government through an Invoice Registration Portal (IRP) before issuing them to buyers. Upon successful validation, the IRP returns a digitally signed invoice with a unique Invoice Reference Number (IRN) and QR code.

Prior to E-Invoicing, businesses manually created invoices in their ERP or billing software and only later reported them in GST returns. This manual approach often led to data mismatches, erroneous ITC claims, and fraudulent invoices. E-Invoicing was introduced to eliminate these gaps by making electronic reporting standard, compulsory (for applicable taxpayers), and near real-time.

The Goal of E-Invoicing

The primary objectives of implementing E-Invoicing are:

- Eliminate fake invoices and reduce tax evasion

- Automate reconciliation between sales invoices and GST returns

- Reduce manual errors and re-work during return filing

- Enable real-time data validation and reporting

- Improve compliance visibility for businesses and government

In essence, E-Invoicing standardizes how invoices are generated, shared, stored, and reported in the GST eco-system.

Historical Evolution of Turnover Thresholds

E-Invoicing was introduced in a phased manner in India, starting with large taxpayers and gradually extending to smaller businesses. This approach allowed businesses to adapt and transition without sudden compliance shock.

Below is an illustrative timeline:

| Phase | Turnover Threshold | Effective From |

|---|---|---|

| Phase I | Rs 500 crore | Oct 2020 |

| Phase II | Rs 100 crore | Jan 2021 |

| Phase III | Rs 50 crore | Apr 2021 |

| Phase IV | Rs 20 crore | Apr 2022 |

| Phase V | Rs 10 crore | Oct 2022 |

| Phase VI | Rs 5 crore | Aug 2023 |

At present, any GST-registered business with an aggregate turnover exceeding ?5 crore must generate e-invoices for its applicable transactions.

This threshold applies to the aggregate turnover — meaning the combined turnover across all GST registrations under the same PAN in India.

Who Needs E-Invoicing?

E-Invoicing is mandatory for:

Businesses With Annual Aggregate Turnover > Rs 5 Crore

If your business, across all GSTINs under one PAN, exceeds ?5 crore in turnover in any previous financial year (from FY 2017-18 onward), you need to generate e-invoices for applicable supplies.

Businesses Making B2B & Export Supplies

E-Invoicing applies to:

- B2B supplies

- Exports of goods/services

- Interstate supplies where applicable

B2C invoices — such as retail bills to consumers — are generally not included in the e-invoicing mandate (but may be if future phases expand applicability).

Who Is Currently Exempt?

- Businesses with turnover below Rs 5 crore

- Purely B2C businesses (no B2B supplies)

- Some specified categories as per GST notifications

Note: Some businesses that cross the threshold mid-year must start e-invoicing from the following financial year. The government provides clarity on this via official circulars and FAQs.

How E-Invoicing Works — Step by Step

The E-Invoicing process may seem complex at first, but it’s essentially a standardized data flow between your billing system and the government portal.

Step 1 — Create an Invoice in Your System

You generate an invoice in your accounting, ERP, or billing software as usual.

Step 2 — Submit to the Invoice Registration Portal (IRP)

You send the invoice data electronically to the IRP. This can be done via:

- API integration from your ERP

- GSP (GST Suvidha Provider)

- Bulk upload (JSON or CSV)

Step 3 — Validation by IRP

The IRP verifies mandatory fields including:

- GSTIN of supplier and recipient

- HSN codes

- Taxable value

- Tax amounts

- Invoice date and number

If valid, an Invoice Reference Number (IRN) and a QR code are issued.

Step 4 — Receive Signed E-Invoice

The IRP returns a digitally signed invoice with IRN & QR code.

Step 5 — Issue to Buyer & Record

You download the signed e-invoice and share it with the customer. The invoice data automatically flows into the GST system and, in some cases, the e-way bill system.

Important: Once an IRN is generated, the invoice cannot be edited. To make corrections, a cancellation and reissue process must be followed.

Key Components of an E-Invoice

A compliant GST E-Invoice must include:

Supplier details (Name, GSTIN, place of supply)

Customer details (Name, GSTIN if supplied)

Unique invoice number and date

Description, quantity, value of goods/services

HSN/SAC codes

Tax rates and amounts (CGST/SGST/IGST/UTGST)

IRN and QR code

Missing or incorrect data often leads to rejection by the IRP — which emphasizes the need for standardized invoice formats.

Example: E-Invoicing Data Flow

Let’s visualize how data flows during e-invoicing:

- Invoice Generated in ERP →

- Data Sent to IRP →

- IRP Validates & Returns IRN →

- Signed Invoice Shared with buyer →

- Data Flows to GST Portal for return reconciliation

This automated cycle eliminates manual GST return entries and significantly reduces compliance fatigue.

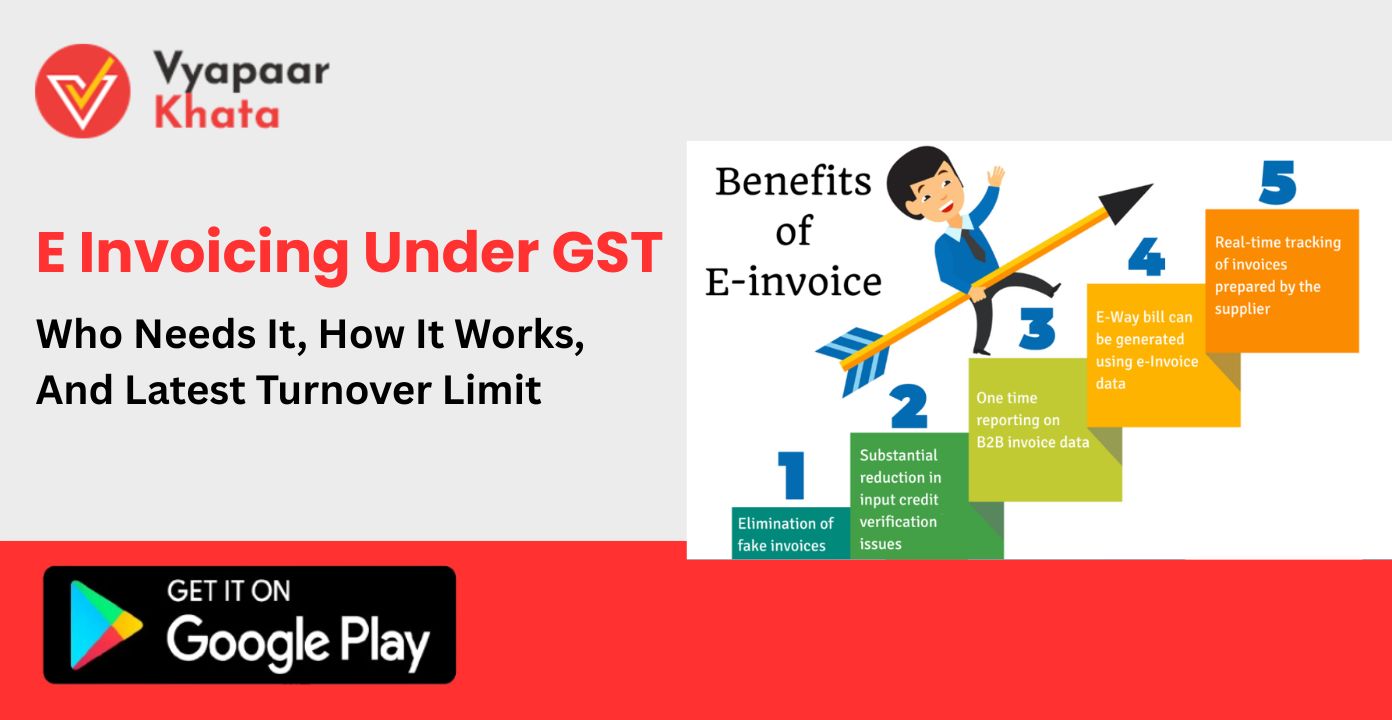

Why E-Invoicing Matters (Benefits)

1. Accuracy and Automation

Manual entry errors — a major cause of mismatches between invoices and GST returns — get eliminated.

2. Faster GST Return Filing

Once invoices are reported to IRP, details auto-populate in GST returns such as GSTR-1 (Sales), reducing filing time.

3. Improved Input Tax Credit (ITC) Matching

Since invoice data flows directly to the GST system, buyers receive accurate and validated data, which improves ITC claims.

4. Reduced Tax Evasion & Fraud

Real-time submission makes it harder to create fake invoices or duplicate records.

5. Better Compliance Monitoring

Government and businesses get better visibility into transaction data, leading to smarter policy and analytics.

6. Simplified E-Way Bill Generation

For goods transportation, many businesses find e-way bills can now generate more seamlessly with IRN data.

30-Day Upload Rule (Effective April 1, 2025)

Starting April 1, 2025, a new rule mandates that:

Taxpayers with aggregate turnover above Rs 10 crore must upload e-invoices (including credit/debit notes) to the IRP within 30 days from the invoice date.

Invoices submitted after 30 days will be rejected by the portal, making timely reporting crucial.

For taxpayers with turnover between Rs 5 crore and Rs 10 crore, there’s no mandatory 30-day rule yet — though timely reporting is always recommended.

Integrating E-Invoicing With Accounting Systems

Most modern accounting or ERP systems now offer API plug-ins or built-in GST e-invoice modules.

Key Integration Approaches:

- Built-in E-Invoice API with GSTN/IRP

- GST Suvidha Provider (GSP) Based Integration

- Batch Upload (for small businesses)

Good integration ensures:

Automatic IRN generation

Auto-sync with sales and GST returns

Fewer manual steps

At the larger scale, enterprises integrate e-invoice submission, GST returns and e-way bill systems for full automation.

VyapaarKHATA — Simplifying E-Invoicing and Beyond

In the complex world of GST compliance, VyapaarKHATA stands out as a simple and powerful solution for managing invoice, billing, and accounting — all in one place.

VyapaarKHATA helps businesses to:

- Create GST & Non-GST invoices and bills

- Send invoices via email and WhatsApp

- Manage customer contacts

- Handle inventory management

- Track purchase orders and purchases

- Monitor expenses and financial records

VyapaarKHATA is designed for today’s MSME and SME ecosystem, which comprises over 63 million businesses in India alone. At VyapaarKHATA, the mission is straightforward: to build practical, affordable, and intuitive digital tools that empower small and medium enterprises to grow without being bogged down by complexity.

Why VyapaarKHATA Matters:

- Works across B2B and B2C invoicing

- Supports inventory and expense tracking

- Enables GST-compliant documentation

- Helps even non-technical users manage accounting with ease

By combining compliance readiness with powerful business management features, VyapaarKHATA reduces administrative overhead — letting entrepreneurs focus on growth instead of form filling.

Consequences of Non-Compliance

Failing to meet e-invoicing requirements can lead to:

Invalid Tax Documentation

Invoices not reported through the IRP may not qualify as valid GST documents — putting ITC eligibility at risk for buyers.

Penalties & Interest

Errors, delays, or non-compliance attract interest on GST liabilities and penalties under the GST Act.

Audit and Notices

Inaccurate or missing invoices may trigger compliance notices, prolonged audits, and enforcement scrutiny.

Timely, accurate reporting isn’t just about avoiding penalties — it protects your financial credibility and business reputation.

Common Challenges and How to Overcome Them

Confusion Over Threshold Calculation

Many businesses fail to grasp that aggregate turnover includes all GSTINs under the same PAN.

Solution: Maintain accurate GSTIN-level reporting and check applicable thresholds annually.

Missing Mandatory Fields

Invoices rejected due to missing HSN codes or mismatched GSTIN entries.

Solution: Use standard invoice templates and validation before submission.

Late Uploads

Missing the 30-day window (for > ?10 crore turnover) leads to rejections.

Solution: Automate reporting through APIs or software with reminders.

Data Sync With GST Returns

Sometimes the GST portal doesn’t auto-populate data as expected.

Solution: Review return drafts and reconcile IRP data with ERP systems.

Best Practices for E-Invoicing Compliance

Validate Invoice Data Before Submission

Ensure GSTIN, HSN codes, values, and dates are accurate.

Standardize Invoice Numbers

Use consistent numbering to reduce mismatches.

Automate Integration With ERP

Manually uploading invoices increases the risk of delays and errors.

Train Your Team

Ensure accounting and finance teams understand GST e-invoice rules.

Reconcile Regularly

Monthly reconciliation helps catch errors before return filing.

Future of E-Invoicing in India

GST e-invoicing continues to evolve:

Wider applicability to new business categories

Further automation between GST, e-way bill and return filing

Enhanced analytics for government and businesses

Possible reduction of turnover thresholds in the future

These changes will only deepen the role of digital compliance in India’s tax ecosystem — making early adoption and strong systems even more important.

Real-World Impact: A Case Illustration

Business A has an aggregate turnover of ?12 crore. Before e-invoicing, sales invoices often showed mismatches between buyer GST returns and the seller’s sales reports.

Post compliance:

Data flows directly to GST systems

ITC claims increase because buyers get validated invoices

Fewer manual corrections in GSTR-1 and GSTR-3B

This reduces compliance cost, improves cash flow, and strengthens tax transparency.

FAQs on E-Invoicing Under GST

Does e-invoicing apply to export invoices?

Yes, export B2B invoices must be reported.

Do I need an e-invoice for retail B2C sales?

Generally no — unless notified otherwise.

Can I edit an invoice after IRN is generated?

No. You must cancel and reissue the invoice.

Is inventory management tied to e-invoice reporting?

Not mandatory, but linking systems improves accuracy.

E-Invoicing is not just another compliance exercise — it is a gateway to a more accurate, transparent, and automated taxation environment.

With the threshold now at ?5 crore, many SMEs and MSMEs need to understand, adopt, and integrate e-invoicing into their billing systems. The transition may pose challenges initially, but with proper systems, strong data discipline, and tools like VyapaarKHATA, businesses can simplify the process and gain long-term benefits.

Whether you are a tax professional, business owner, or accounting partner, the message is clear:

E-Invoicing is here to stay — and the sooner you master it, the better positioned your business will be for growth and compliance in the digital age.

If you’d like, I can also provide infographics, templates, compliance checklists, or video summaries to help you implement e-invoicing smoothly!